Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

U.K. Retail Sales YoY (SA) (Jan)

U.K. Retail Sales YoY (SA) (Jan)A:--

F: --

France Manufacturing PMI Prelim (Feb)

France Manufacturing PMI Prelim (Feb)A:--

F: --

P: --

France Services PMI Prelim (Feb)A:--

F: --

P: --

France Composite PMI Prelim (SA) (Feb)A:--

F: --

P: --

Germany Composite PMI Prelim (SA) (Feb)

Germany Composite PMI Prelim (SA) (Feb)A:--

F: --

P: --

Germany Manufacturing PMI Prelim (SA) (Feb)A:--

F: --

P: --

Germany Services PMI Prelim (SA) (Feb)A:--

F: --

P: --

Euro Zone Composite PMI Prelim (SA) (Feb)

Euro Zone Composite PMI Prelim (SA) (Feb)A:--

F: --

P: --

Euro Zone Manufacturing PMI Prelim (SA) (Feb)A:--

F: --

P: --

Euro Zone Services PMI Prelim (SA) (Feb)A:--

F: --

P: --

U.K. Manufacturing PMI Prelim (Feb)A:--

F: --

P: --

U.K. Services PMI Prelim (Feb)A:--

F: --

P: --

U.K. Composite PMI Prelim (Feb)A:--

F: --

P: --

India Deposit Gowth YoY

India Deposit Gowth YoYA:--

F: --

P: --

Mexico Economic Activity Index YoY (Dec)

Mexico Economic Activity Index YoY (Dec)A:--

F: --

P: --

Canada Retail Sales MoM (SA) (Dec)

Canada Retail Sales MoM (SA) (Dec)A:--

F: --

Canada Core Retail Sales MoM (SA) (Dec)A:--

F: --

P: --

ECB Chief Economist Lane Speaks U.S. IHS Markit Services PMI Prelim (SA) (Feb)

U.S. IHS Markit Services PMI Prelim (SA) (Feb)A:--

F: --

P: --

U.S. IHS Markit Manufacturing PMI Prelim (SA) (Feb)A:--

F: --

P: --

U.S. IHS Markit Composite PMI Prelim (SA) (Feb)A:--

F: --

P: --

U.S. UMich Consumer Sentiment Index Final (Feb)A:--

F: --

P: --

U.S. Existing Home Sales Annualized Total (Jan)A:--

F: --

U.S. UMich Consumer Expectations Index Final (Feb)A:--

F: --

P: --

U.S. UMich Current Economic Conditions Index Final (Feb)A:--

F: --

P: --

U.S. Existing Home Sales Annualized MoM (Jan)A:--

F: --

U.S. UMich 1-Year-Ahead Inflation Expectations Final (Feb)A:--

F: --

P: --

BOC Gov Macklem Speaks U.S. Weekly Total Oil Rig CountA:--

F: --

P: --

U.S. Weekly Total Rig CountA:--

F: --

P: --

BOC Press Conference Turkey Capacity Utilization (Feb)

Turkey Capacity Utilization (Feb)--

F: --

P: --

Indonesia Loan Growth YoY (Jan)

Indonesia Loan Growth YoY (Jan)--

F: --

P: --

Germany Ifo Business Expectations Index (SA) (Feb)--

F: --

P: --

Germany Ifo Current Business Situation Index (SA) (Feb)--

F: --

P: --

Germany IFO Business Climate Index (SA) (Feb)--

F: --

P: --

Euro Zone Core CPI Final MoM (Jan)--

F: --

P: --

Euro Zone CPI YoY (Excl. Tobacco) (Jan)--

F: --

P: --

Euro Zone Core HICP Final YoY (Jan)--

F: --

P: --

Euro Zone HICP MoM (Excl. Food & Energy) (Jan)--

F: --

P: --

Euro Zone HICP Final YoY (Jan)--

F: --

P: --

Euro Zone HICP Final MoM (Jan)--

F: --

P: --

Euro Zone Core HICP Final MoM (Jan)--

F: --

P: --

Euro Zone Core CPI Final YoY (Jan)--

F: --

P: --

Canada National Economic Confidence Index--

F: --

P: --

U.S. Chicago Fed National Activity Index (Jan)--

F: --

P: --

U.S. Dallas Fed New Orders Index (Feb)--

F: --

P: --

U.S. Dallas Fed General Business Activity Index (Feb)--

F: --

P: --

U.S. 2-Year Note Auction Avg. Yield--

F: --

P: --

South Korea Benchmark Interest Rate

South Korea Benchmark Interest Rate--

F: --

P: --

Germany GDP Revised YoY (Working-day Adjusted) (Q4)--

F: --

P: --

Germany GDP Final YoY (Not SA) (Q4)--

F: --

P: --

Germany GDP Final QoQ (SA) (Q4)--

F: --

P: --

U.K. CBI Retail Sales Expectations Index (Feb)--

F: --

P: --

U.K. CBI Distributive Trades (Feb)--

F: --

P: --

U.S. Weekly Redbook Index YoY--

F: --

P: --

U.S. FHFA House Price Index (Dec)--

F: --

P: --

U.S. FHFA House Price Index YoY (Dec)--

F: --

P: --

U.S. S&P/CS 20-City Home Price Index MoM (SA) (Dec)--

F: --

P: --

U.S. S&P/CS 20-City Home Price Index YoY (Not SA) (Dec)--

F: --

P: --

U.S. FHFA House Price Index MoM (Dec)--

F: --

P: --

No matching data

US

US VN

VN TW US VN TW

TW US VN TWLatest Views

Latest Views

Trending Topics

To quickly learn market dynamics and follow market focuses in 15 min.

In the world of mankind, there will not be a statement without any position, nor a remark without any purpose.

Inflation, exchange rates, and the economy shape the policy decisions of central banks; the attitudes and words of central bank officials also influence the actions of market traders.

Money makes the world go round and currency is a permanent commodity. The forex market is full of surprises and expectations.

Top Columnists

Enjoy exciting activities, right here at FastBull.

The latest breaking news and the global financial events.

I have 5 years of experience in financial analysis, especially in aspects of macro developments and medium and long-term trend judgment. My focus is maily on the developments of the Middle East, emerging markets, coal, wheat and other agricultural products.

BeingTrader chief Trading Coach & Speaker, 8+ years of experience in the forex market trading mainly XAUUSD, EUR/USD, GBP/USD, USD/JPY, and Crude Oil. A confident trader and analyst who aims to explore various opportunities and guide investors in the market. As an analyst I am looking to enhance the trader’s experience by supporting them with sufficient data and signals.

Latest Update

Risk Warning on Trading HK Stocks

Despite Hong Kong's robust legal and regulatory framework, its stock market still faces unique risks and challenges, such as currency fluctuations due to the Hong Kong dollar's peg to the US dollar and the impact of mainland China's policy changes and economic conditions on Hong Kong stocks.

HK Stock Trading Fees and Taxation

Trading costs in the Hong Kong stock market include transaction fees, stamp duty, settlement charges, and currency conversion fees for foreign investors. Additionally, taxes may apply based on local regulations.

HK Non-Essential Consumer Goods Industry

The Hong Kong stock market encompasses non-essential consumption sectors like automotive, education, tourism, catering, and apparel. Of the 643 listed companies, 35% are mainland Chinese, making up 65% of the total market capitalization. Thus, it's heavily influenced by the Chinese economy.

HK Real Estate Industry

In recent years, the real estate and construction sector's share in the Hong Kong stock index has notably decreased. Nevertheless, as of 2022, it retains around 10% market share, covering real estate development, construction engineering, investment, and property management.

Hongkong, China

Ho Chi Minh, Vietnam

Dubai, UAE

Lagos, Nigeria

Cairo, Egypt

White Label

Data API

Web Plug-ins

Affiliate Program

View All

No data

English

English Español

Español العربية

العربية Bahasa Indonesia

Bahasa Indonesia Bahasa Melayu

Bahasa Melayu Tiếng Việt

Tiếng Việt ภาษาไทย

ภาษาไทย Français

Français Italiano

Italiano Türkçe

Türkçe Русский язык

Русский язык 简中

简中 繁中

繁中Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up

Hongkong, China

Ho Chi Minh, Vietnam

Dubai, UAE

Lagos, Nigeria

Cairo, Egypt

White Label

Data API

Web Plug-ins

Affiliate Program

BOE Governor Bailey said at the Jackson Hole Economic Symposium on August 23 that he thought long-term inflation pressures were easing but further interest rate cuts would not be rushed.

Traders appear to be stepping back from last Friday’s risk-on rally, showing more caution in the Asian session today. The mood in major indices is mixed; with Nikkei trading down by more than -1%, while HSI is showing gain of about 1%. This cautious sentiment is mirrored in the currency markets, where safe-haven currencies like Yen and Swiss Franc have gained slightly alongside Dollar. Risk-sensitive currencies like Aussie and Kiwi are losing some ground.

However, the movements are relatively muted, with no major technical levels being breached. This suggests that markets are merely in a phase of consolidation, indicating that markets are in a holding pattern, digesting recent moves and waiting for the next catalyst.

Today’s economic calendar is relatively light, with Germany’s Ifo Business Climate Index and US Durable Goods Orders being the primary data points to watch. With the UK on a bank holiday, trading might remain subdued for now. But things are expected to pick up as the week progresses, especially with upcoming inflation data from the US, Eurozone, Japan, and Australia.

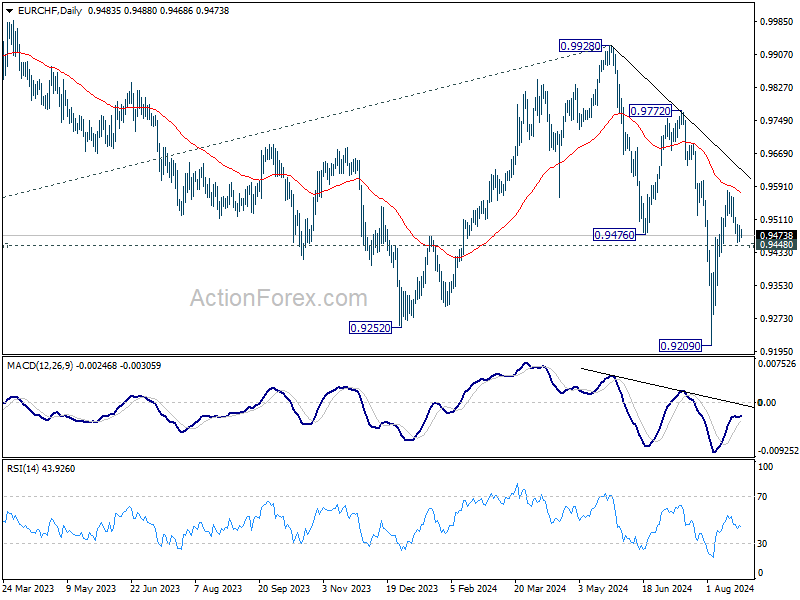

Technically, EUR/CHF would be a focus today. While the rebound from 0.9209 was strong, it struggled to break through 55 D EMA (now at 0.9577). Decisive break of 0.9448 minor support will argue that this rebound has completed after reject by the 55 D EMA. That would keep the down trend from 0.9928 intact too, and could set the stage for retesting 0.9209 low next.

In Asia, at the time of writing, Nikkei is down -1.09%. Hong Kong HSI is up 1.00%. China Shanghai SSE is down -0.07%. Singapore Strait Times is up 0.01%. Japan 10-year JGB yield is down -0.0162 at 0.879.

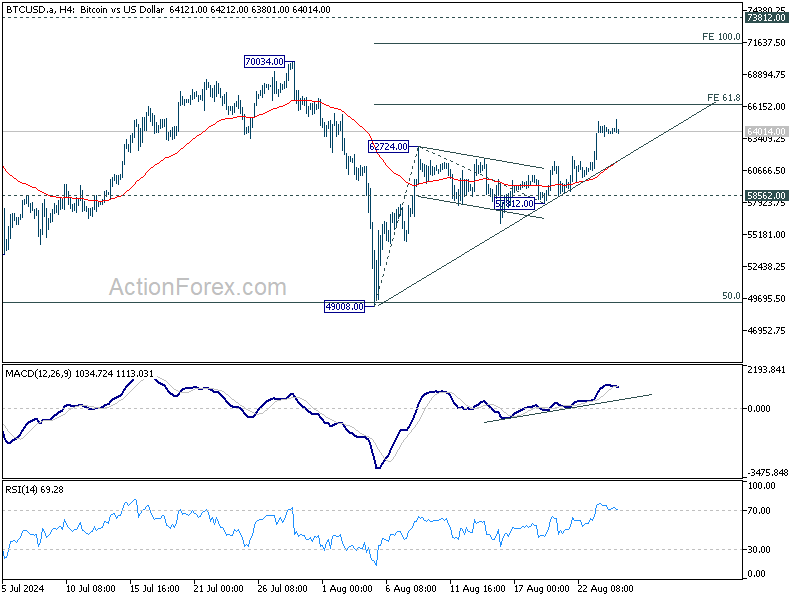

Bitcoin surged last Friday and stayed firm throughout the weekend. The cryptocurrency broke through an important near-term resistance level, fueled by broad risk-on sentiment following Fed Chair Jerome Powell’s indication of upcoming monetary easing. It now stands at a critical juncture, where the next move will determine whether it has completed the medium-term consolidation that began in March.

Technically, the break of 62724 confirmed resumption of the rebound from 49008. The strong break of 55 D EMA is also a near term bullish sign. It’s possible that the corrective pattern from 73812 has completed 49008, after hitting 50% retracement of 24896 to 73812 at 49354.

However, to solidify the bullish case, Bitcoin will have to overcome the first hurdle at 61.8% projection of 49008 to 62724 from 57812 at 66288. Rejection by this level will keep the rebound from 49008 as just another leg in the corrective pattern from 73812. On the other hand, firm break of 66288 could prompt upside acceleration to 100% projection at 71528, and build up momentum for eventual breakout from the five-month range.

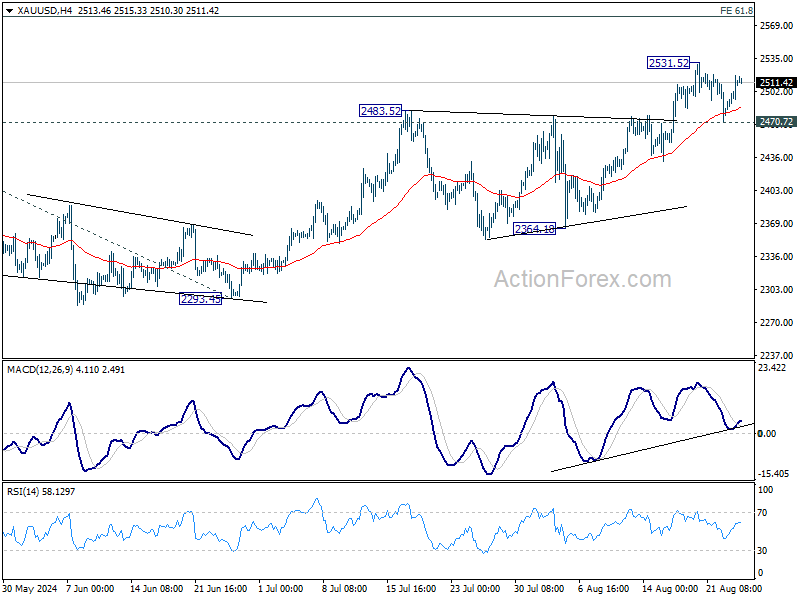

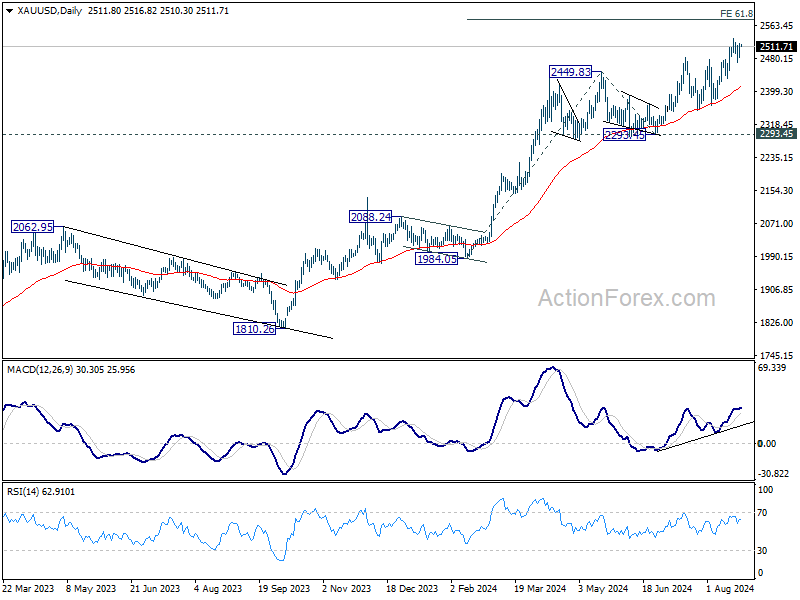

Both Gold and Silver are currently still caught in near-term consolidations despite the rally late last week. Both metals have the potential to extend their recent gains, but a more pronounced decline in Dollar may be necessary to provide the needed momentum.

As for Gold, further rally is expected as long as 2470.72 support holds. Firm break of 2531.57 will resume the long term up trend and extend the record run. Next target is 61.8% projection of 1984.05 to 2449.83 from 2293.45 at 2581.30. However, break of 2470.72 will risk deeper pull back to 55 D EMA (now at 2412.87) first.

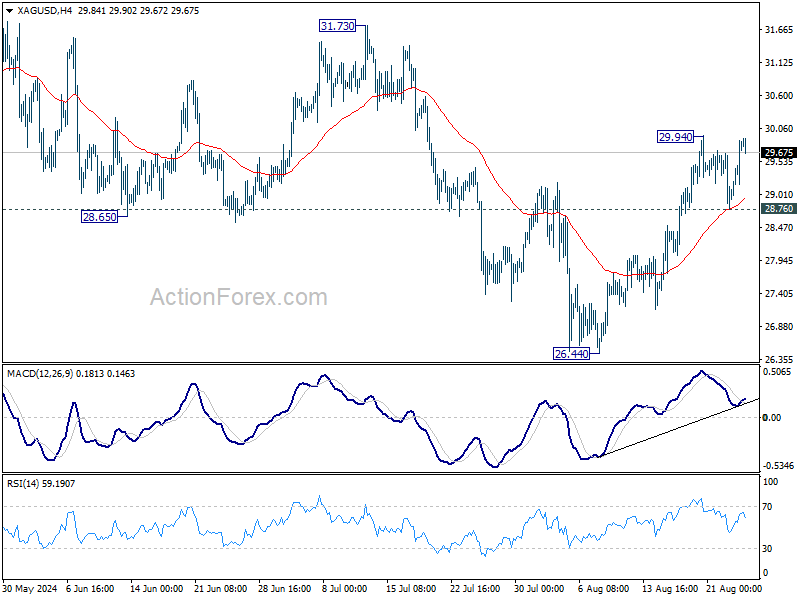

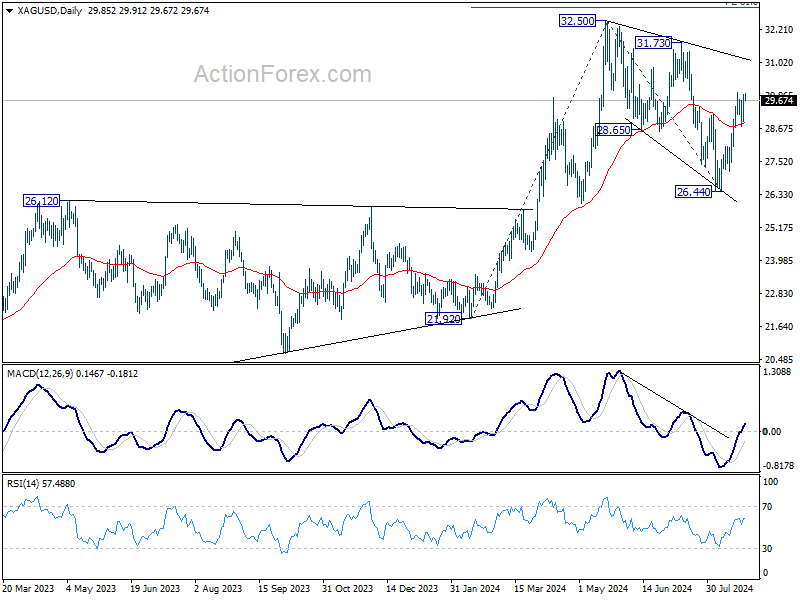

While Silver has been lagging Gold in its run, there is prospect of a catch up ahead. Corrective pattern from 32.50 has likely completed with three waves down to 26.44, after defending 26.12 resistance turned support. For now, further rise is in favor as long as 28.76 support holds. Break of 29.94 will target 31.73 resistance. Decisive break there will solidify this view and target 32.50 and above. However, break of 28.76 will dampen this immediate bullish case.

Inflation data will remain the focal point for the markets this week. In the US, PCE inflation report is set to take the spotlight. This report is anticipated to strengthen the case for a rate cut by Fed in September, a move that Fed Chair Jerome Powell has already hinted at. However, with another round of NFP and CPI data due before the next FOMC meeting, the exact size of the initial rate cut remains uncertain. Despite this, Fed officials appear to leans towards cautious, measured approach. So, barring any shocks, a 25 bps is the more probable outcome. Alongside inflation, the markets will also be watching data on durable goods orders, GDP revisions, and personal income and spending.

Eurozone’s CPI flash estimate is expected to be a pivotal piece of data that could seal the deal for a rate cut by ECB in September. This would mark the second cut in the current cycle. Meanwhile, Eurozone’s economic outlook is clouded by concerns over Germany slipping back into a recession. The Ifo business climate index and GfK consumer sentiment survey, thus, will be closely watched for signs of deteriorating confidence in Europe’s largest economy.

In Japan, Tokyo CPI report, often seen as a precursor to national inflation trends, will be a key focus. It may be too early to determine if BoJ will hike rates again this year. Upcoming data on industrial production and retail sales will be crucial. These figures could provide insight into whether rebound of Japan’s industrial sector is gaining momentum in the second half of the year and whether earlier wage increases are translating into higher consumer spending sustainably.

Meanwhile, in Australia, the monthly CPI is expected to show a notable slowdown. However, unless the data reveals significant downside surprises, RBA is likely to hold off on cutting rates this year. Retail sales data from Australia will also be monitored for further clues about consumption trends.

Monday: Germany Ifo business climate; US durable goods orders.

Tuesday: Japan corporate service prices; Germany GDP final; US house price index, consumer confidence.

Wednesday: Australia monthly CPI; Germany Gfk consumer sentiment; Swiss UBS economic expectations; Eurozone M3 money supply.

Thursday: New Zealand ANZ business confidence; Japan consumer confidence; Germany CPI flash; US GDP revision, jobless claims, goods trade balance, pending home sales.

Friday: Japan Tokyo CPI, unemployment rate, industrial production, retail sales, housing starts; Australia retail sales; Germany import prices, unemployment; French consumer spending; Swiss KOF economic barometer; UK M4 money supply, mortgage approvals; Eurozone CPI flash unemployment rate; Canada GDP; US personal income and spending; PCE inflation, Chicago PMI.

This approach has, at this time, brought investors' inflationary expectations down to 2.1 percent for the next five- to ten-year period.

So, Fed actions in this part of the financial markets have seemingly convinced the investment community that the Fed is serious about achieving the Fed's 2.0 percent target for inflation in the economy.

But, this is not all that the Federal Reserve has done over the past twenty-nine months. The Federal Reserve has also conducted a policy of quantitative tightening, where it has worked to reduce the size of the Fed's securities portfolio.

Here is the Fed's performance over the past twenty-nine months. The total reduction in the Federal Reserve portfolio has been just under $1.8 trillion. As can be seen, this reduction has occurred in a very steady and persistent manner.

Economists and market participants are getting worried over the possibility of a recession happening because of what the Federal Reserve has done.

As readers of my posts know, I am not as concerned with this possibility because of all the money the Federal Reserve pumped into the economy as it was fighting the disturbances caused by the Covid-19 pandemic and following recession.

I believe that we need to add a few earlier months to the above chart.

This picture, I believe, puts the current reduction in the M2 money stock into the proper perspective.

The compound annual rate of growth of the M2 money stock during this time of expansion is over 8.0 percent.

Historically, this puts the current period into the class of "excessive" monetary growth.

The only reason, seemingly, that inflation did not get more "out-of-hand" is that people did not use the money stock at the same pace that they formerly had done. That is the velocity of monetary circulation fell.

Although the velocity of circulation of the M2 money stock has picked up, it has still not returned to earlier levels.

As a consequence, as I have frequently been writing about, there is a lot of money "lying around" in the financial system.

For example, the commercial banking system has about $3.3 trillion in "vault cash."

This is one reason that the U.S. economy is still performing at a relatively satisfactory rate, and it is also the reason why the stock market has hit all the "historic highs" it did while the Federal Reserve was conducting a policy of quantitative tightening.

In fact, Mr. Powell, in his Jackson Hole speech, reviews the state of the economy and professes that the economy is in a relatively good place.

Economic growth, according to Mr. Powell, "continues...at a solid pace."

"Prices have risen 2.5 percent over the past 12 months."

"The labor market has cooled considerably from its formerly overheated state." This is the result of "a substantial increase in the supply of workers and a slowdown from the previously frantic pace of hiring." Not that bad.

So, the economy is in pretty good shape, but there are issues in the financial sector that need to be dealt with.

It is a time for policy adjustment.But, Mr. Powell reiterates, the Federal Reserve should not go overboard in trying to get everything right in the next few months.

The Federal Reserve will move...but, just don't expect it to move too rapidly.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

White Label

Data API

Web Plug-ins

Poster Maker

Affiliate Program

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.