Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Signal Accounts for Members

All Signal Accounts

All Contests

U.K. Trade Balance Non-EU (SA) (Oct)

U.K. Trade Balance Non-EU (SA) (Oct)A:--

F: --

P: --

U.K. Trade Balance (Oct)A:--

F: --

P: --

U.K. Services Index MoMA:--

F: --

P: --

U.K. Construction Output MoM (SA) (Oct)A:--

F: --

P: --

U.K. Industrial Output YoY (Oct)A:--

F: --

P: --

U.K. Trade Balance (SA) (Oct)A:--

F: --

P: --

U.K. Trade Balance EU (SA) (Oct)A:--

F: --

P: --

U.K. Manufacturing Output YoY (Oct)A:--

F: --

P: --

U.K. GDP MoM (Oct)A:--

F: --

P: --

U.K. GDP YoY (SA) (Oct)A:--

F: --

P: --

U.K. Industrial Output MoM (Oct)A:--

F: --

P: --

U.K. Construction Output YoY (Oct)A:--

F: --

P: --

France HICP Final MoM (Nov)

France HICP Final MoM (Nov)A:--

F: --

P: --

China, Mainland Outstanding Loans Growth YoY (Nov)

China, Mainland Outstanding Loans Growth YoY (Nov)A:--

F: --

P: --

China, Mainland M2 Money Supply YoY (Nov)A:--

F: --

P: --

China, Mainland M0 Money Supply YoY (Nov)A:--

F: --

P: --

China, Mainland M1 Money Supply YoY (Nov)A:--

F: --

P: --

India CPI YoY (Nov)

India CPI YoY (Nov)A:--

F: --

P: --

India Deposit Gowth YoYA:--

F: --

P: --

Brazil Services Growth YoY (Oct)

Brazil Services Growth YoY (Oct)A:--

F: --

P: --

Mexico Industrial Output YoY (Oct)

Mexico Industrial Output YoY (Oct)A:--

F: --

P: --

Russia Trade Balance (Oct)

Russia Trade Balance (Oct)A:--

F: --

P: --

Philadelphia Fed President Henry Paulson delivers a speech

Philadelphia Fed President Henry Paulson delivers a speech Canada Building Permits MoM (SA) (Oct)

Canada Building Permits MoM (SA) (Oct)A:--

F: --

P: --

Canada Wholesale Sales YoY (Oct)A:--

F: --

P: --

Canada Wholesale Inventory MoM (Oct)A:--

F: --

P: --

Canada Wholesale Inventory YoY (Oct)A:--

F: --

P: --

Canada Wholesale Sales MoM (SA) (Oct)A:--

F: --

P: --

Germany Current Account (Not SA) (Oct)

Germany Current Account (Not SA) (Oct)A:--

F: --

P: --

U.S. Weekly Total Rig CountA:--

F: --

P: --

U.S. Weekly Total Oil Rig CountA:--

F: --

P: --

Japan Tankan Large Non-Manufacturing Diffusion Index (Q4)

Japan Tankan Large Non-Manufacturing Diffusion Index (Q4)--

F: --

P: --

Japan Tankan Small Manufacturing Outlook Index (Q4)--

F: --

P: --

Japan Tankan Large Non-Manufacturing Outlook Index (Q4)--

F: --

P: --

Japan Tankan Large Manufacturing Outlook Index (Q4)--

F: --

P: --

Japan Tankan Small Manufacturing Diffusion Index (Q4)--

F: --

P: --

Japan Tankan Large Manufacturing Diffusion Index (Q4)--

F: --

P: --

Japan Tankan Large-Enterprise Capital Expenditure YoY (Q4)--

F: --

P: --

U.K. Rightmove House Price Index YoY (Dec)--

F: --

P: --

China, Mainland Industrial Output YoY (YTD) (Nov)--

F: --

P: --

China, Mainland Urban Area Unemployment Rate (Nov)--

F: --

P: --

Saudi Arabia CPI YoY (Nov)

Saudi Arabia CPI YoY (Nov)--

F: --

P: --

Euro Zone Industrial Output YoY (Oct)

Euro Zone Industrial Output YoY (Oct)--

F: --

P: --

Euro Zone Industrial Output MoM (Oct)--

F: --

P: --

Canada Existing Home Sales MoM (Nov)--

F: --

P: --

Euro Zone Total Reserve Assets (Nov)--

F: --

P: --

U.K. Inflation Rate Expectations--

F: --

P: --

Canada National Economic Confidence Index--

F: --

P: --

Canada New Housing Starts (Nov)--

F: --

P: --

U.S. NY Fed Manufacturing Employment Index (Dec)--

F: --

P: --

U.S. NY Fed Manufacturing Index (Dec)--

F: --

P: --

Canada Core CPI YoY (Nov)--

F: --

P: --

Canada Manufacturing Unfilled Orders MoM (Oct)--

F: --

P: --

Canada Manufacturing New Orders MoM (Oct)--

F: --

P: --

Canada Core CPI MoM (Nov)--

F: --

P: --

Canada Manufacturing Inventory MoM (Oct)--

F: --

P: --

Canada CPI YoY (Nov)--

F: --

P: --

Canada CPI MoM (Nov)--

F: --

P: --

Canada CPI YoY (SA) (Nov)--

F: --

P: --

Canada Core CPI MoM (SA) (Nov)--

F: --

P: --

No matching data

Latest Views

Latest Views

Trending Topics

Top Columnists

Latest Update

White Label

Data API

Web Plug-ins

Affiliate Program

View All

No data

As Gold faces the challenge of a corrective decline, driven by a return to long-duration risk assets and equities, investors are closely watching key technical levels. The metal's traditional role as a stagflation hedge is questioned, with geopolitical stability and market shifts impacting its safe haven appeal. The article delves into the charts, highlighting crucial support and resistance levels, providing insights into potential scenarios that may shape Gold's near-term trajectory.

_1")

_2")

_3")

_4")

_5")

_6")

_7")

_8")

_9")

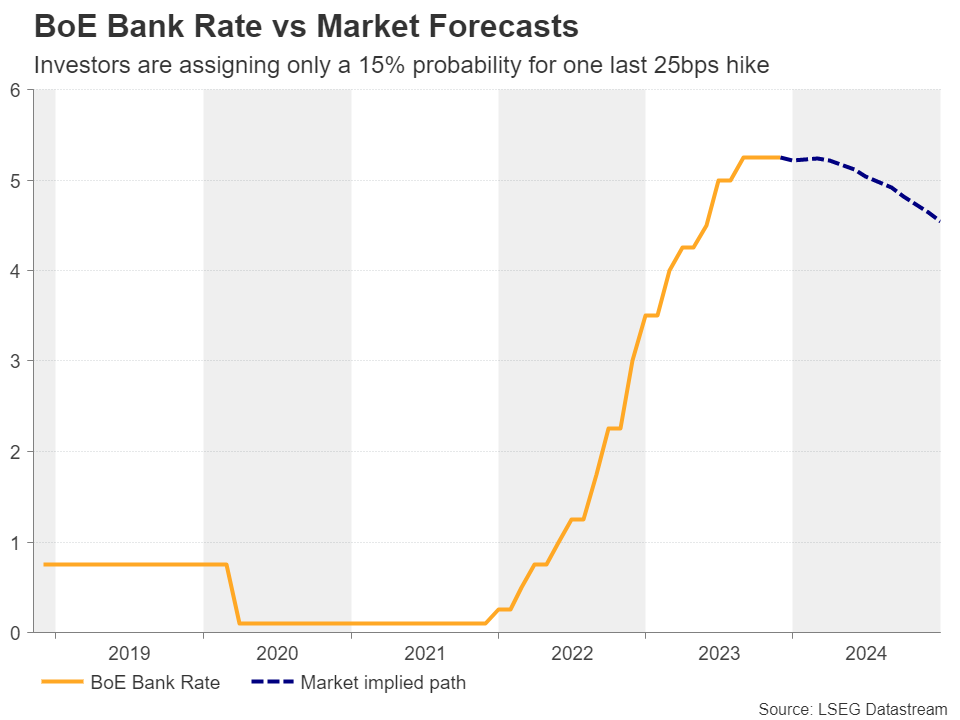

Last week, the Bank of England decided to keep interest rates unchanged via a 6-3 vote, with the three dissenters favoring a 25bps hike. In the accompanying statement, officials noted that policy must stay restrictive for an extended period, and that further tightening may be required if there is evidence of more persistent inflationary pressures. At the press conference, Governor Bailey said that inflation is still too high and that they are determined to take it all the way down to 2%, adding to the decision’s hawkish flavor.

That said, even after the BoE’s ‘higher for longer’ message, investors continue to see only a 15% probability for another quarter point hike by February and around 70bps worth of rate cuts by the end of next year.

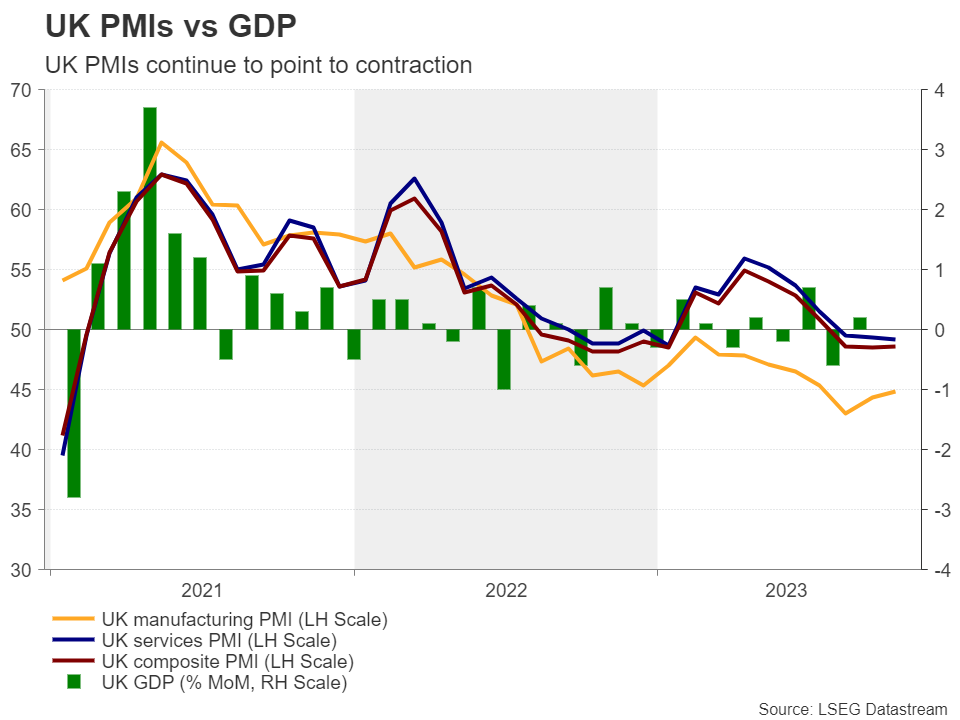

Did the UK economy contract in Q3?

With the Bank estimating flat economic growth for Q3 this year, Friday’s official GDP data for the quarter may attract special interest. Expectations are for the economy to have shrunk 0.1% q/q after growing 0.2% q/q in Q2, with a contraction supported by the UK composite PMI, which fell from 50.8 in July to 48.6 in August and then to 48.5 in September.

A negative growth rate could confirm the market’s view that BoE policymakers may be forced to press the cut button earlier than they currently believe, bringing the pound under selling interest. That said, the British currency may not suffer huge losses if the contraction is mild as traders may decide to save ammunition for next week’s employment and inflation data, on Tuesday and Wednesday respectively. For investors to sell the pound and forget next week’s releases, the GDP growth rate may need to miss the forecast by a decent margin.

Given that Governor Bailey said after last week’s meeting that whether GDP growth is slightly negative or slightly positive will not impact monetary policy, next week’s data may prove more important in shaping expectations about the Bank’s future plans if indeed the GDP figure comes in at -0.1%.

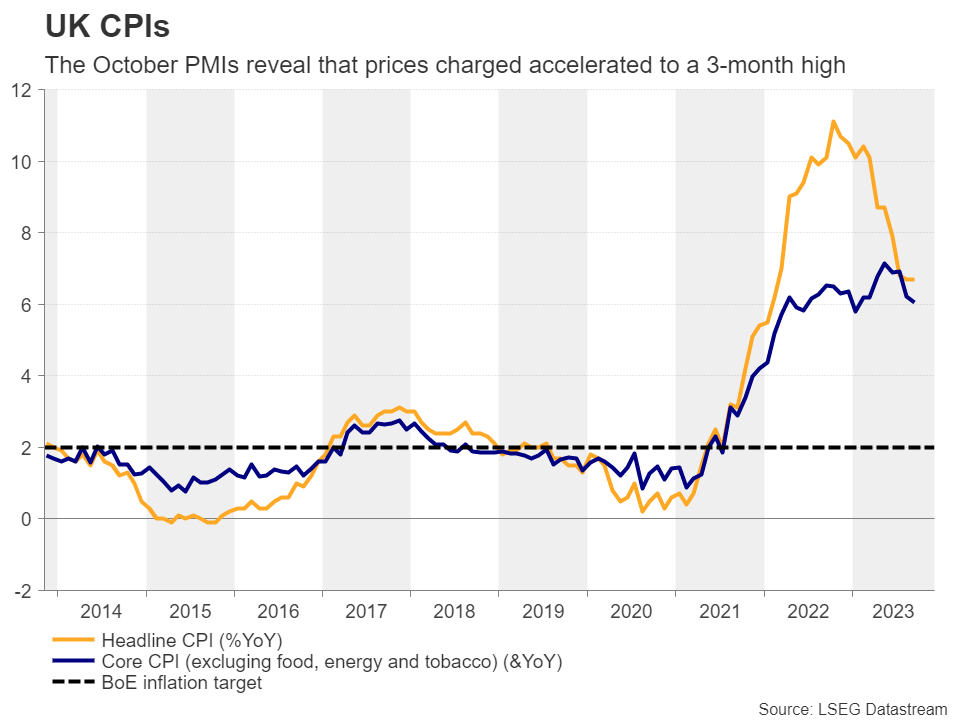

Both the headline and core CPI rates are more than three times the BoE’s target of 2%, which means that policymakers’ mission is far from accomplished and that indeed some further tightening may be needed, despite market participants not sharing that view. According to the UK PMIs for the month, prices charged by companies accelerated to a three-month high in October, tilting the risks surrounding the CPI report to the upside.

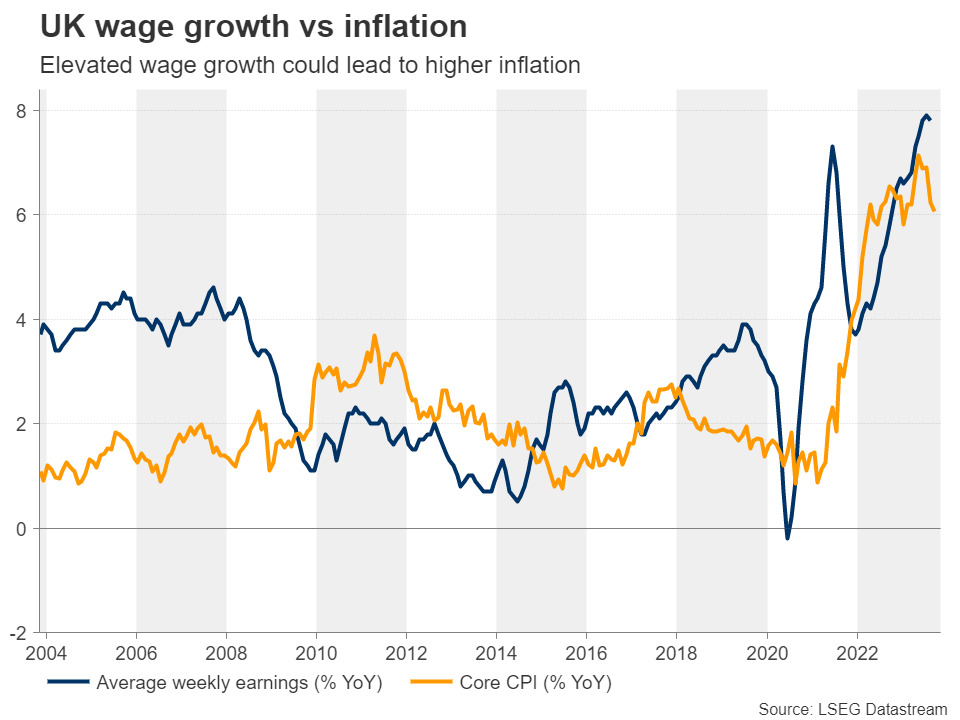

On the other hand, the KPMG and REC UK report on jobs pointed to a further easing of overall pay growth, which means that Tuesday’s data may reveal a slowdown in average weekly earnings. Having said that, a small slowdown in the excluding bonuses rate from 7.8% is unlikely to be a reason for complacency. For investors to maintain a low probability for another rate hike by the BoE and keep several rate cuts for next year on the table, the CPIs on Wednesday may need to reveal a slowdown as well, or the wage growth rate may need to slide to levels that will raise speculation of lower inflation in future months, even if Wednesday’s CPI rate sees as small rebound.

Cable rallied on Friday following the disappointing US employment report, but with the US dollar staging a shy comeback this week, the pair returned below the key territory of 1.2310. If the GDP data suggests that the economy contracted by more than anticipated, the pair is likely to continue drifting south, especially if wages slow as well next Tuesday. However, whether the slide will extend to reach the round figure of 1.2000 may depend on Wednesday’s CPI data.

For the pair to return above 1.2310 and perhaps violate its 200-day moving average, even if economic growth and wages slow somewhat, the inflation data may need to reveal a rebound in both the headline and core rates. In such a case, the bulls may feel confident to climb towards the 1.2600 zone.

Curve inversion/outperformance of the long end was the name of the game on core bond markets yesterday. US yields ceded between 1.4 bps (2-y) and 11 bps (30-y). The US 10-y yield closed near the key 4.50% reference. German yields showed a similar picture. The 2-y still gained 3.1 bps but the 30-y declined 8.1 bps. The German 10-y yield at 2.62% also closed below the 2.68% neckline, suggesting more downside might be on the cards short-term. The rise of short-term EMU yields was at least partially explained by the ECB consumer expectations survey. EMU consumers in September expected a sharp rise for the year ahead inflation at 4.0% vs 3.5% in August. If this trend persists, it gives the ECB little room to mitigate its anti-inflation campaign. At the same time, consumers turned more negative on the economy and on the labour market over the next 12 months. Uncertainty on (global) growth probably is a driver for recent rebound in bonds with long maturities. ECB speakers (Lane, Nagel, Vujcic, Makhlouf) yesterday at least kept the focus on inflation rather than on growth and indicated that it’s too early to start the debate on (potential) easing. The oil price continued its downtrend, which also might have supported momentum in bonds with longer maturities. Brent oil even closed below $80 p/b. On other markets, European equities enjoyed a constructive momentum. The EuroStoxx 50 gained 0.6% (and off the intraday peak levels). US indices showed no clear trend ending little changed. On FX markets, the dollar gave up early gains. DXY closed little changed at 105.6. After testing the 1.066 area, EUR/USD at 1.071 even closed with a small gain. USD/JPY still was the exception to the rule with the closing just below the 151 big figure. EUR/GBP regained the 0.87 barrier as markets ponder recent comments from the likes of BoE chief economist Pill on the timing of a potential BoE rate cut mid next year.

Asian equities indices mostly trade in positive territory this morning. China underperforms. China CPI (-0.2% Y/Y) and PPI (-2.6% Y/Y) moved (further) into deflation territory, suggesting a mediocre growth momentum. US Treasuries are trading little changed and so does the dollar (DXY 105.55, EUR/USD 1.071). Later today, weekly US jobless claims are interesting and might give some guidance for the intraday momentum on bond markets but evidently is no game changer. Central bank speak will again dominate market headlines, with plenty of ECB and Fed governors giving their view, including ECB Chair Lagarde and Fed Chair Powell. ECB speakers recently mostly pushed back against bets that tightening is done and we don’t expect that to change anytime soon. Fed Powell will speak at an IMF conference debating monetary policy challenges in the global economy. Markets will look out for his assessment on financial conditions after recent market repositioning. A wait-and-see attitude in current environment might extend the bond market rebound and be a tentative negative for the dollar. The US Treasury also will sell $24 bln 30-y bonds.

Data from the US Department of Agriculture showed average prices of beef sold in US shops and supermarkets rising to nearly $8 per pound, a record high. Live cattle prices trade near $1.8 per pound at the Chicago Mercantile Exchange, also near highs ($1.87). Years of low rainfall and rising costs for hay and other feeds used for fattening in absence of grass pushed farmers to reduce their cattle stocks. Arabica coffee prices rose to their highest level since June (topping $1.7 per pound) despite good crops in top exporter Brazil. As stronger Brazilian real and port congestion (delay shipments) might be at play. Soy bean prices rose to their highest level since mid-September ($13.85 a bushel) on the back of strong Chinese demand and on fears that dry weather in the northwest of Brazil could reduce production over there.

Minutes of the previous Bank of Canada policy meeting showed that policy makers were split on the need of an additional rate hike following their October pause at 5%. They are keeping the door open as the transmission from higher rates to weaker growth and lower inflation is rather slow. Officials raised their expectations for inflation in the near term, saying higher oil prices, rent and housing costs and the slow normalization of corporate pricing are limiting the disinflation process. They also noted elevated inflation expectations and wage growth. Canadian money markets think we’ve seen peak rates with a first policy rate cut discounted by early H2 next year.

USDJPY is looking to resume its bullish trend ahead of Powell’s speech, having softly pivoted near the 149.30 level at the start of the week.

To attract new buyers, the bulls will have to surpass the nearby resistance of 151.65 and move beyond the 2022 top of 151.93. In this case, the price could pick up steam towards the important resistance trendline area at 153.00. Another successful battle there could see the price jumping into the 155.40-156.60 constraining zone taken from March-June 1990.

However, the mixed technical indicators do not convince traders of the bullish scenario. The narrowing Bollinger bands indicate a potential explosive move but the direction is unclear as the rising RSI has recently escaped a drop below its 50 neutral mark, whereas the MACD keeps lacking power below its red signal line.

Hence, a downside correction could still be possible in the coming sessions. If the pair slumps below the 149.00-149.50 range formed by the short-term ascending trendline from September and the 50-day simple moving average (SMA), it could stabilize near the 148.30 mark. Otherwise, the sell-off could expand towards the 146.55-147.30 territory. Yet only a clear close below the lower boundary of the broad bullish channel at 145.65 would disappoint medium-term traders.

Summing up, USDJPY has not eliminated downside risks yet, despite marking a positive week. To boost buying confidence, the pair will need to crawl above 151.93, and more importantly, strengthen its uptrend above 153.00. In such a case, though, it is worth considering that a sharp depreciation in the yen could prompt another round of FX intervention by Japanese authorities.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

White Label

Data API

Web Plug-ins

Poster Maker

Affiliate Program

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up